For investors looking to diversify and grow their wealth beyond traditional stocks and bonds, real estate, specifically multifamily, has emerged as a compelling asset class, offering the potential for steady income, capital appreciation, and resilience against market volatility.

Effective portfolio construction hinges on understanding true risk tolerance—both financially and emotionally—more than just age or time horizon. This understanding enables the creation of a plan that balances growth potential with the ability to weather market fluctuations.

Brokerage accounts and traditional retirement vehicles such as 401(k)s and IRAs rely heavily on stocks and bonds. They face limitations such as market volatility, limited income potential, and fixed yields vulnerable to inflation.

There are different real estate investment options, such as REITs, private funds, and syndications, each with distinct risk-reward profiles.

Multifamily real estate can provide current income and capital appreciation, in addition to low correlation with stocks and bonds, smoothing overall portfolio volatility.

Funds provide broad exposure and stability, while single asset partnerships offer focused exposure to high conviction opportunities.

Assessing Your Risk Tolerance and Investment Goals

Portfolio construction begins with a thorough understanding of personal risk tolerance and investment goals. While age and time horizon are factors, capturing the full picture of risk tolerance involves assessing both financial ability to absorb losses and emotional ability to endure the inevitable market fluctuations. Investment goals, meanwhile, vary widely, from building wealth for future generations to generating steady income in retirement.

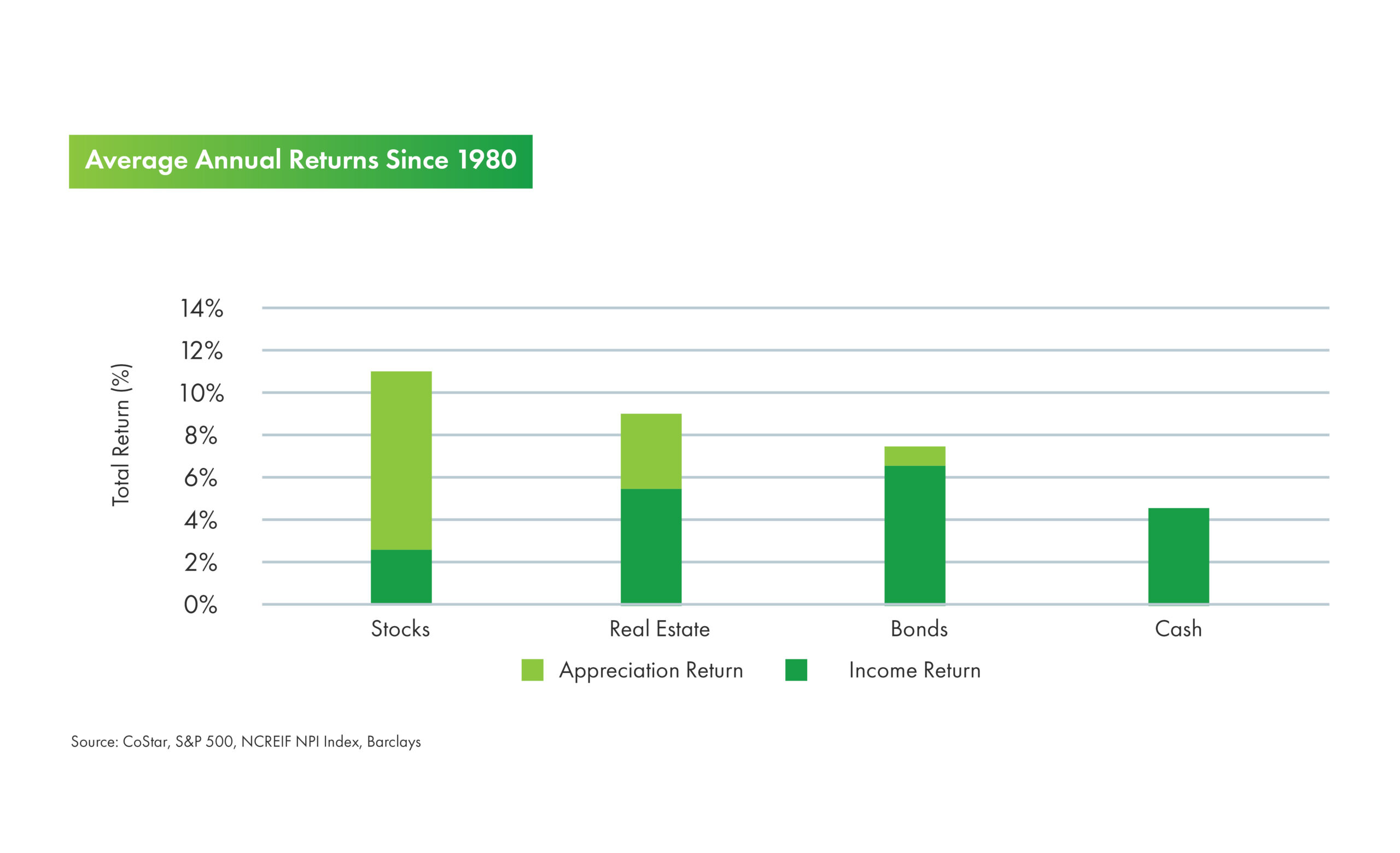

For many investors, traditional asset classes like common stocks provide a benchmark for assessing risk and return potential. The S&P 500, a broad index of U.S. equities, has historically delivered strong annualized returns over the last 25 years. However, these returns have been accompanied by multiple corrections (declines of 10% or more) and bear markets (declines of 20% or more), including the dot-com crash of 2000-2002 and the global financial crisis of 2008-2009.

Commercial real estate, by contrast, has shown more stability. Over the same 25-year period, real estate values have generally trended upward with fewer sharp downturns.

Leverage and Diversification

Leverage, or borrowing capital to amplify investment returns, can significantly shape risk and reward in real estate. Investing with managers who employ conservative leverage represents one way to reduce risk in real estate. For example, a property financed with a 50% loan-to-value (LTV) ratio is less vulnerable to market dips than one leveraged at 80%. Excess leverage can raise returns but leaves assets exposed when rents soften or property values decline.

Diversification across geographies offers another layer of protection against risks such as regional economic slowdowns. A manufacturing downturn in one region may not affect tech-driven growth in another. Income-focused strategies, such as investing in stabilized multifamily properties with strong cash flow, often carry a lower risk profile than growth-oriented approaches like speculative development.

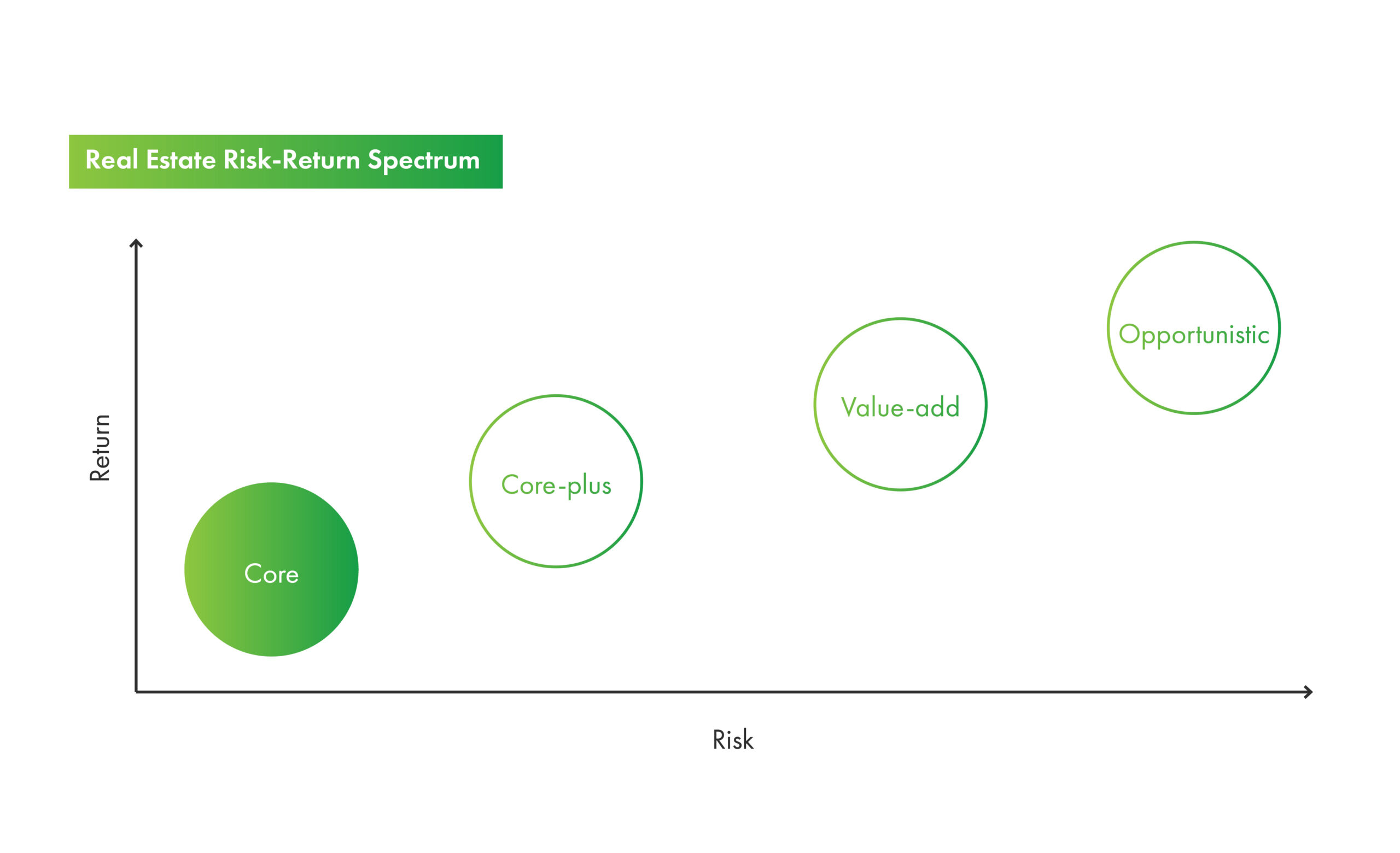

Multifamily Strategies and Returns

Core strategies focus on acquiring stabilized, high-quality properties in prime locations, characterized by consistent rental income and minimal operational challenges. Leases are backed by high-credit tenants, offering moderate, predictable appreciation, making them suitable for investors prioritizing capital preservation and stable cash flow.

Value-add strategies target properties with untapped potential, often involving older or under-managed assets that require major renovations and operational improvements to enhance their market value. Investors aim to increase rental income and achieve substantial appreciation through the execution of the business plan.

Opportunistic strategies pursue high-risk, high-reward opportunities, such as ground-up development, distressed property acquisitions, or significant redevelopment projects. These strategies may be subject to entitlement risk, construction risk, interest rate risk, capital markets risk, and lease-up risk. Accordingly, the expected return for this type of strategy is commensurately higher than alternative lower-risk strategies.

Limitations of Traditional Retirement Vehicles

Volatility and Inflation Challenges

Traditional retirement vehicles, such as 401(k)s and IRAs, often rely heavily on equities and fixed-income securities. While equities have historically provided growth, they are susceptible to significant downside risk during market downturns. Fixed-income securities, such as bonds, may offer stability, but their yields may not keep pace with inflation, potentially eroding purchasing power over time. Multifamily real estate offers a compelling alternative. Rent growth has historically tracked or exceeded inflation.

Growth vs. Current Income

Retirement portfolios often prioritize growth over yield, requiring retirees to draw down their principal for income. This approach can be problematic during periods of market volatility, as declining asset values can accelerate the depletion of retirement savings. Multifamily real estate, on the other hand, can deliver dependable cash flows through rental income, providing a more stable source of retirement income.

Correlation

Conventional assets, such as stocks and bonds, tend to move in tandem with market trends, offering limited diversification benefits. Private equity real estate, particularly multifamily, exhibits a lower correlation with equities, offering a potential hedge against market volatility. During periods of economic uncertainty, rental income from multifamily properties may remain relatively stable, even as equity markets experience significant fluctuations.

Tax Advantages

Real estate investments can provide tax benefits absent in traditional vehicles. While REIT dividends face ordinary income taxes, private multifamily investments structured as pass-through entities benefit from the deduction of deprecation and other non-cash charges, enhancing after-tax returns.

Understanding Real Estate Investment Options

Direct Ownership

Owning a property outright grants full control: Deciding tenants, upgrades, and sales timing. It also entails significant operational responsibilities, from maintenance to evictions, so scaling beyond a few properties becomes impractical for most.

Real Estate Investment Trusts (REITS)

Public Real Estate Investment Trusts (REITs) trade on a stock exchange and offer liquidity and dividend yields, making them an attractive option for some investors. However, REITs are often more correlated with equities than private real estate investments, making them susceptible to market volatility. Additionally, REITs may trade at a discount to their net asset value (NAV), and their fee structures can erode returns.

Private Real Estate Funds

Private real estate funds offer professionally managed portfolios of high-quality assets, providing accredited investors with access to diversified real estate investments. These funds typically require longer commitment periods, but transparent reporting and expert due diligence can appeal to investors seeking scale without hands-on involvement.

Syndicators

Syndicators pool capital for individual multifamily properties. While many are qualified, inexperienced sponsors may lack expertise, leading to poor underwriting and lower investment performance. They may have minimal co-investment and oftentimes prioritize immediate fees over the long-term performance of the investment.

Crowdfunding

Crowdfunding platforms connect investors (capital) to sponsors and offer lower minimum investment thresholds — making real estate investments accessible to a wider range of investors. However, these platforms often involve less transparency, higher fees, and little alignment between the sponsor and the crowdfunding platform.

How Real Estate Fits into a Diversified Portfolio

Volatility Reduction

Real estate, particularly multifamily, can play a crucial role in a diversified investment portfolio. Its low correlation with stocks and bonds can help reduce overall portfolio volatility. This characteristic becomes especially valuable during periods of economic turbulence. For instance, during the 2020 COVID-19 market crash, the S&P 500 plummeted 34% in a matter of weeks, while multifamily rents in many markets held steady or even increased as demand for rental housing surged amid economic uncertainty.

Data suggests a portfolio with a 15% allocation to real estate can reduce standard deviation (a measure of volatility) by 1-2% compared to a traditional 60/40 stock-bond mix. Consider a $1 million portfolio: a 60/40 allocation might exhibit annual volatility of 10%, translating to potential swings of $100,000. Adding a 15% multifamily allocation could trim that volatility to 8-9%.

Income and Appreciation

Multifamily real estate’s dual role as an income generator and appreciation vehicle sets it apart from many asset classes. Rental income provides reliable cash flows, often yielding 5-8% annually on invested capital, depending on market conditions and property type. Appreciation, meanwhile, offers a secondary growth engine. Multifamily values have climbed steadily—averaging 3-4% annually over 20 years, driven by the steady growth in operating incomes and new construction costs.

Limited Partner Investing in Real Estate

Structure and Benefits

Limited partner (LP) investing in real estate is a suitable option for accredited investors seeking exposure to the asset class without the operational burdens of direct ownership. LP investments provide access to professionally managed portfolios of high-quality assets, with general partners (GPs) overseeing acquisitions, management, and dispositions. Multifamily LP investments may offer average internal rates of return (IRRs) of 8-12%, including distributions on paid-in capital (DPI) reflecting the cash returned to investors. Professional management ensures rigorous due diligence—GPs analyze market data, tenant trends, and cap rates—while economies of scale reduce costs like maintenance or financing. Tax advantages, including depreciation and interest deductions, further enhance after-tax returns.

Liquidity and Time Horizon

LP investments are illiquid by design, with capital typically committed for around 10 years, requiring a long-term investment horizon. This long-term commitment aligns with real estate’s long-term value creation timeline, and minimizes transaction costs. Some funds maybe offer liquidity mechanisms: secondary markets let LPs sell stakes to other investors, or redemption clauses after a hold period.

Vetting General Partners

Selecting the right general partner (GP) is crucial in successful real estate investing. GPs are the stewards of investor capital— tasked with sourcing, managing, and exiting investments—making their expertise, alignment, and execution track record critical to delivering superior risk-adjusted returns. A GP’s track record is the foundation of credibility. Focus on those with a minimum of 10-15 years of operational experience and a portfolio of $100 million to $500 million in completed transactions.

Look to the consistency of their performance across market cycles. Real estate is local and GPs should have a presence in their target markets. Additionally, GPs committing meaningful co-investment (5-10%) signals conviction and ties their financial upside to investment performance. Utilize references with past LPs to assess what numbers can’t capture.

Fund Investments vs. Single Asset Investments

Fund investments provide broad diversification across multiple properties and markets, potentially reducing risk. This diversification can mitigate the impact of any single property’s performance on the overall portfolio. Funds are designed to allow investors to access a portfolio of assets that would be difficult to assemble individually.

Single asset investments, on the other hand, offer the potential for higher returns due to the concentrated nature of the investment. If the property performs well, investors can realize significant gains. However, single asset investments also carry higher risk, as the performance of the investment is tied to the success of a single property.

Individuals (i.e., natural persons) may qualify as accredited investors based on wealth and income thresholds, as well as other measures of financial sophistication.

Financial Criteria

Net worth over $1 million, excluding primary residence (individually or with spouse or partner), or;

Income over $200,000 (individually) or $300,000 (with spouse or partner) in each of the prior two years, and reasonably expects the same for the current year

Professional Criteria

Investment professionals in good standing holding the general securities representative license (Series 7), the investment adviser representative license (Series 65), or the private securities offerings representative license (Series 82)

For further specifications please refer to the SEC website

Stay up to date.

Subscribe to receive the latest news and insights from our team, event invitations, and opportunities to invest.

Leverage and Diversification

Leverage and Diversification